The funding options, the term sheet traps, the dilution math, and the FEMA rules,- everything an Indian founder needs to raise smart, not just raise fast.

Most Founders Raise Money. Smart Founders Raise It on Their Terms.

Two Indian companies. Two very different outcomes.

Zerodha never raised a single rupee of institutional capital. Nithin and Nikhil Kamath bootstrapped it from a small office in Bangalore. By 2025, it was generating over Rs 4,200 crore in annual profits. The founders still own the company outright. No investors. No board seats given away. No liquidation preferences to navigate. Full control, full upside.

BYJU’S raised over $4.5 billion across multiple rounds from marquee global investors. At its peak, it was valued at $22 billion. But the fundraising terms grew increasingly founder-hostile with each round — heavy debt obligations, aggressive investor interventions, and governance structures that progressively stripped the founder’s control. By 2024, the company was in insolvency proceedings, and the founder’s stake was effectively worthless.

The difference was not the business model. It was how capital was raised,- and on whose terms.

This guide is not about convincing you to raise money. It is about making sure that if you do, you keep enough of what you built to make it worth the effort.

7 Ways to Fund Your Business, And What Each Costs You in Control

Every funding source comes with a price. Sometimes that price is interest. Sometimes it is equity. And sometimes it is your ability to make decisions in the company you built. Here is the honest comparison:

| Source | How It Works | Dilution | Control Impact | Best For |

| Bootstrapping | Your own savings, reinvested profits | Zero | Full control retained | Early stage. Revenue-generating businesses. Founders who want independence. |

| Angel Investors | HNIs invest Rs.25L-2Cr for equity. Networks: Indian Angel Network, Mumbai Angels, LetsVenture. | 10-25% at seed | Minimal,- angels rarely take board seats | Post-MVP stage. Need smart money + mentorship + network. |

| Venture Capital | VC funds invest Rs.2Cr-100Cr+ for significant equity. Series A onwards. | 15-25% per round | Board seat(s). Veto rights on key decisions. Information rights. | High-growth companies ready to scale fast. Need large capital. |

| Private Equity | PE firms invest Rs.50Cr+ for majority or significant minority. Later stage. | 20-51%+ | Significant. Often take operational control. | Mature, profitable businesses. Pre-exit growth capital. |

| Bank / NBFC Loans | Term loans and working capital. RBI-regulated. Collateral often required. | Zero equity dilution | No control impact. But personal guarantees common. | Asset-backed businesses. Revenue-stage companies with cash flow. |

| Venture Debt | Debt from specialised funds (Trifecta, Alteria, InnoVen). Typically alongside equity round. | Minimal,- small warrant coverage | No board seats. But covenants and repayment obligations. | Extending runway between equity rounds without extra dilution. |

| Govt Schemes | MUDRA (up to Rs.20L), CGTMSE (collateral-free up to Rs.10Cr since April 2025), Startup India Seed Fund, Fund of Funds. | Zero | Zero | Micro/small businesses. Early-stage DPIIT-recognised startups. |

| THE QUESTION MOST FOUNDERS SKIP Before approaching any business investor, ask: do I actually need equity capital, or do I need working capital? If your business generates revenue and you need money to bridge cash flow gaps or fund inventory, a bank loan or venture debt may cost you zero equity. Too many founders give away 15-25% of their company to solve a problem that a Rs.50 lakh working capital loan could have fixed. |

If you do decide to raise equity, the next thing you need to understand, before a single conversation with an investor, is the term sheet. Because the terms matter more than the valuation.

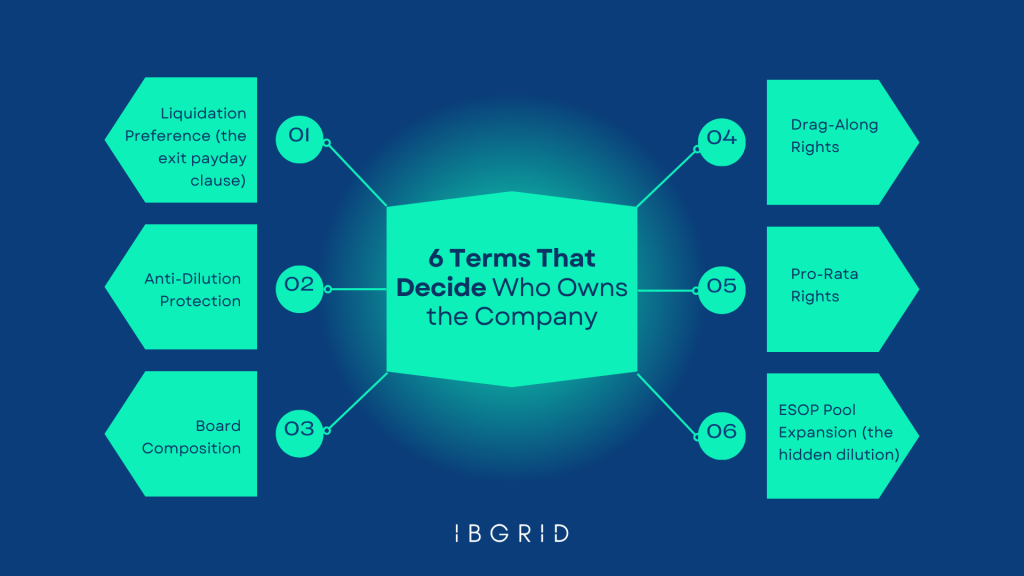

The Term Sheet: 6 Terms That Decide Who Really Owns Your Company

| “Understand what is consideration given to stockholders versus what is given as retention or earn-out packages. Be particularly aware of liquidation preferences and map out in advance what will happen.” By Lightspeed Venture Partners India, Based on interviews with Indian founders across Rs.25,000+ crore in aggregate exits, Lightspeed India Source:Lightspeed India Blog |

A term sheet is the document that outlines the key terms of an investment before the detailed agreements are drafted. It is typically non-binding on price,- but binding on the terms that determine your future control, economics, and flexibility. Here are the six terms that matter most:

1. Liquidation Preference (the exit payday clause):

Determines who gets paid first when the company is sold. A 1x non-participating preference means the investor gets their money back first, then the remaining proceeds are split by ownership. A 1x participating preference means the investor gets their money back first AND a pro-rata share of everything that remains. On a Rs.50 crore exit with Rs.15 crore invested at 1x participating, the investor takes Rs.15 crore off the top, then 30% of the remaining Rs.35 crore (another Rs.10.5 crore),- totalling Rs.25.5 crore on a Rs.15 crore investment, leaving you with Rs.24.5 crore instead of Rs.35 crore.

2. Anti-Dilution Protection:

Protects the investor if you raise a future round at a lower valuation (a ‘down round’). Full ratchet anti-dilution is the harshest,- it reprices all of the investor’s shares to the new lower price, massively diluting founders. Weighted average is softer and more common. Always push for broad-based weighted average. Full ratchet can be devastating.

3. Board Composition:

Who sits on your board controls your company’s strategic decisions. Investors typically want at least one board seat. The key negotiation: ensure founders retain majority board control (e.g., 2 founder seats + 1 investor seat + 1 independent). Losing board majority means losing veto power on hiring, spending, and exit decisions.

4. Drag-Along Rights:

Allows majority shareholders (often investors after multiple rounds) to force all shareholders,- including founders,- to sell. This means if your investors want to exit at a price you think is too low, you may have no choice but to sell. Negotiate a minimum floor price or a founder consent threshold.

5. Pro-Rata Rights:

Gives existing investors the right to invest in future rounds to maintain their ownership percentage. Not inherently bad,- but when combined with aggressive anti-dilution, it can lock founders into a cycle where investors maintain ownership while founders keep getting diluted.

6. ESOP Pool Expansion (the hidden dilution):

Investors often require you to expand your ESOP pool before their investment,- meaning the dilution comes from your shares, not theirs. A typical ask is 10-15% ESOP pool created from the pre-money cap table. This is standard, but negotiate the size carefully. Every extra percent comes out of your pocket, not the investor’s.

The Dilution Math Nobody Shows You

Here is what actually happens to your ownership across three rounds of funding:

| INR DILUTION EXAMPLE Starting point: You and your co-founder own 100%. You set aside 10% for an ESOP pool. Founder ownership: 90%. Seed Round: You raise Rs.1 crore at Rs.5 crore pre-money valuation. Investor gets 16.7%. Your ownership drops to 75%. Series A: You raise Rs.10 crore at Rs.40 crore pre-money. Investor gets 20%. But before the round, the new investor requires a 5% ESOP pool expansion from pre-money. Your ownership drops to 57%. Series B: You raise Rs.30 crore at Rs.120 crore pre-money. Investor gets 20%. Another 3% ESOP expansion. Your ownership: 43%. After three rounds, you own 43% of a company valued at Rs.150 crore. Your 44.2% is worth Rs.66 crore on paper. If the terms are clean (non-participating preference), this is a genuine Rs.64.5 crore position. If you accepted participating preferred at every round, the investors take their money off the top first,- and your effective take at exit could be 30-40% less than the headline suggests. |

| “Aim for dilution of between 15% and 20% per round. If you’re going way beyond that or doing a lot of rounds, you can get way too diluted and kill your startup’s financing prospects.” By Dan Green, Partner, Gunderson Dettmer (Global Tech Law Firm) Source: Latitud Blog |

The math determines your ownership. But between the term sheet and the money landing in your account, there is a process that takes longer than most founders expect.

What Happens Between ‘Yes’ and Money in Your Account

The investor said yes. The term sheet is signed. The celebration is premature.

Between a signed term sheet and capital hitting your bank account, there are 3-6 months of legal, regulatory, and compliance work. Here is the process:

Stage 1: Due Diligence (2-6 weeks)

The investor’s legal and financial team examines your company,- financials, contracts, IP ownership, cap table, compliance history, pending litigation. This is where surprises kill deals. Clean records accelerate this stage. Messy records can extend it by months or collapse the deal entirely.

Stage 2: Definitive Agreements (3-6 weeks)

Lawyers draft the Share Subscription Agreement (SSA), Shareholders’ Agreement (SHA), and board resolutions. The SHA is the real governance document,- it defines board composition, reserved matters (decisions that require investor consent), exit rights, information rights, and ESOP terms. Negotiate this as carefully as you negotiated the valuation. The terms in the SHA will govern your life as a founder for the next 5-10 years.

Stage 3: Regulatory Filings and Share Allotment (2-4 weeks)

Board resolution approving the allotment. ROC filing (Form PAS-3 within 15 days). If the investor is foreign: FEMA compliance including FCGPR filing with the authorised dealer bank within 30 days. Valuation certificate from a SEBI Merchant Banker or Practising CA must be in place. Share certificates issued. Cap table updated. Only then does the money legally settle.

| REALISTIC TIMELINE Angel round (Indian investor, simple terms): 4-8 weeks from term sheet to money VC round (Indian fund, standard SHA): 8-14 weeks VC round (foreign investor, FEMA compliance): 12-20 weeks Plan your runway accordingly. If you have 6 months of cash left, you needed to start fundraising 3 months ago. |

If Your Investor Is Foreign: The FEMA Rules You Cannot Ignore

Accepting capital from a non-resident investor triggers FEMA compliance. Get this wrong and you face penalties, invalid allotments, and,- in extreme cases,- unwinding of the entire transaction. Here is what applies:

• FDI Pricing Floor: Shares of an unlisted Indian company cannot be issued to a non-resident below fair market value. FMV must be determined by DCF or NAV, certified by a SEBI Merchant Banker or Practising CA. Issue below FMV and the allotment is invalid under FEMA.

• FCGPR Filing: Form FCGPR must be filed with the authorised dealer bank within 30 days of share allotment. Late filing attracts compounding penalties from RBI. Many founders miss this deadline and face expensive remediation later.

• Press Note 3 (2020): If your investor is from a country sharing a land border with India,- China, Pakistan, Bangladesh, Nepal, Myanmar, Bhutan, Afghanistan,- prior government (DPIIT) approval is mandatory, regardless of sector. This adds 3-6 months to the process and applies even if the ultimate beneficial owner is from a border country.

• Sectoral Caps: Some sectors have FDI limits,- insurance (74%), defence (74%), multi-brand retail (51%). Check the DPIIT Consolidated FDI Policy for your sector before accepting foreign capital.

• Downstream Investment: If your company has foreign ownership and invests in another Indian entity, downstream investment rules under FEMA apply. This catches many founders off guard when they set up subsidiaries.

What Fundraising Costs Before You Even Get the Money

Nobody talks about this. Here is what you will spend just to close a funding round:

- Valuation report (IBBI-RV or SEBI MB): Rs.1.5, 5 lakh

- Legal fees (SSA, SHA, board resolutions): Rs.3, 15 lakh (scales with round complexity and number of investors)

- FEMA compliance (if foreign investor): Rs.1, 3 lakh for filings and certifications

- CA/auditor fees for due diligence support: Rs.1, 3 lakh

- Stamp duty on share issuance: Varies by state,- typically 0.005% to 0.1%

Total: Rs.5, 25 lakh in transaction costs before the capital arrives. On a Rs.2 crore angel round, that is 2.5-12.5% of your raise going to lawyers, valuers, and compliance. Factor this into your fundraising target,- raise enough to cover these costs plus your operational needs.

4 Mistakes That Cost Indian Founders Their Companies

| “Valuation before fundraising is not a vanity exercise. It is a control mechanism. It tells you how much equity you are selling and whether your assumptions survive diligence. If you wait until the term sheet lands, you are negotiating with too little preparation and too much pressure.” By DealPlexus, Valuation & Fundraising Advisory, DealPlexus Source: DealPlexus.com (February 2026) |

1. Raising too much, too early, at too high a valuation.

It feels like winning. It is usually the beginning of losing. An inflated early valuation means your next round must be even higher,- or you face a devastating down round that triggers anti-dilution clauses and destroys founder morale. Raise what you need to hit the next meaningful milestone. Not a rupee more.

2. Signing a term sheet without understanding the terms.

Liquidation preferences, participating preferred, full-ratchet anti-dilution,- these are not academic concepts. They directly determine how much money you actually receive when the company is sold. One founder who signed participating preferred across three rounds discovered at exit that the investors took 70% of the proceeds despite owning only 40% of the equity. The headline ownership and the economic reality were completely different numbers.

3. No valuation before the negotiation.

Walking into an investor meeting without an independent valuation means the investor sets the anchor. Their valuation will be optimised for their return, not your ownership. A Rs.1.5-5 lakh valuation report is the cheapest insurance you can buy against giving away too much of your company.

4. Ignoring cap table math through multiple rounds.

Founders who do not model their ownership through future rounds end up shocked at Series B when they discover they own 15% of a company they started with 100%. Every round sets the precedent for the next. Model 3-4 rounds ahead before you agree to terms today.

The 5 Questions Every Founder Asks Before Their First Round

How long does fundraising take in India?

3-6 months from first investor conversation to money in bank for most rounds. Angel rounds can close in 4-8 weeks. VC rounds with foreign investors and FEMA compliance can take 12-20 weeks after the term sheet is signed. Start fundraising when you have 9-12 months of runway remaining,- not 3.

How much dilution is normal per round?

15-20% per round is the healthy benchmark. Founders should aim to retain 50-60% after Series A. If you are giving up more than 25% in any single round, push back on valuation or reduce the round size. Every extra percent compounds through future rounds.

Do I need a valuation report before talking to investors?

Not legally required for the conversation,- but strategically critical. An independent valuation gives you an anchor for negotiation, prevents the investor from setting the price unilaterally, and is required anyway for Companies Act compliance (S.62 preferential allotment) and FEMA pricing (if the investor is foreign). Get it done before you start conversations. Cost: Rs.1.5-5 lakh.

What if I don’t want to give up equity at all?

You have options. Bank loans (collateral-based), NBFC term loans, venture debt (alongside or between equity rounds), government schemes (MUDRA up to Rs.10 lakh, CGTMSE collateral-free up to Rs.10 crore since April 2025), and revenue-based financing. If your business generates predictable revenue, you may not need to sell equity at all. Not every business is a venture-scale startup,- and that is perfectly fine.

When is the right time to raise?

When you have something to show,- traction, revenue, or at minimum a working prototype with early customer validation. Raising on an idea alone is possible but expensive in dilution terms. The more proof you have, the higher your valuation, the less equity you give away. The worst time to raise is when you are about to run out of money,- because desperation is visible, and investors price it in.

| PLANNING TO RAISE CAPITAL? The difference between a good raise and a bad one is not the amount,- it is the terms, the structure, and how much of your company you keep. Book a free 30-minute consultation. We will help you understand your valuation, model the dilution, and prepare for investor conversations with clarity,- not guesswork. No pitch. No obligation. Email: [email protected] | Phone: 8000 422 133 |

One Reply to “A Founder’s Guide to Funding Without Giving Away Your Company”