When planning to sell your company, do you need an investment banker?

Let’s understand when to hire one, when a CA is enough, what they actually do for their fee, and how to avoid the three mistakes that cost Indian business owners crores in the wrong advisory relationship.

You Built the Business. Selling It Is a Completely Different Skill.

You know how to run your company. You know the market, the clients, the numbers. But selling a company is not operating a company. It is a negotiation against professional buyers,- PE firms, corporate acquirers, and strategic investors,- who have done this dozens of times. You are doing it once.

That asymmetry is where value leaks.

| “If you don’t decide what you want from an exit long before you decide you’re done with your business, you won’t walk away with what it’s worth. It’s as simple as that.” By Jean Moncrieff, Serial Founder & Exit Advisor, JeanMoncrieff.com Source: JeanMoncrieff.com |

A structured sale process run by an experienced M&A advisor typically yields 15-25% higher prices than a bilateral negotiation where you are talking to one buyer without competitive tension. On a Rs.25 crore deal, that difference is Rs.3.75-6.25 crore,- far more than the advisor’s fee.

But not every deal needs an advisor. And hiring the wrong one can be worse than hiring none at all. Let’s break this down.

Investment Banker vs M&A Advisor vs CA: Which One Do You Actually Need?

In India, these three terms get used interchangeably. They are not the same. Here is how to match the right professional to your deal size and complexity:

| Professional | Best For | What They Do | Typical Fee |

| CA with M&A experience | Deals below Rs.10 crore. Simple bilateral transactions. | Valuation, basic buyer identification, tax structuring, SPA negotiation support. Usually solo or small-team practice. | Rs.1-5 lakh (flat or milestone-based). No success fee. |

| Boutique M&A Advisor | Deals Rs.10-100 crore. SME and mid-market transactions. | Full process: CIM preparation, buyer identification (20-50 targets), competitive auction, DD management, negotiation, deal structuring, closing coordination. | Retainer: Rs.1-3 lakh/month. Success fee: 2-3% of deal value. Minimum fee: Rs.15-30 lakh. |

| Investment Banker | Deals above Rs.100 crore. Complex, cross-border, or PE-backed transactions. | Everything above, plus: capital raising, regulatory navigation (SEBI, CCI, RBI), institutional buyer access (PE funds, family offices, global corporates), complex deal structuring. | Retainer: Rs.3-10 lakh/month. Success fee: 1-2% of deal value. Minimum fee: Rs.50 lakh-1 crore. |

Pro Tip: The deal-size boundaries are guidelines, not rules. A Rs.15 crore deal with cross-border elements, regulatory complexity, or multiple buyer types may need an M&A advisor even though the value is ‘small.’ Complexity, not just size, determines who you need.

Now that you know who to hire, here is what they actually do once you engage them.

What an M&A Advisor Actually Does (7 Things You Cannot Do Yourself)

1. Confidential Information Memorandum (CIM).

The CIM is the document that tells your company’s story to potential buyers,- financials, growth drivers, market position, competitive advantages, and investment thesis. A good CIM makes buyers compete for your business. A bad one makes them pass. Writing your own CIM is like writing your own resume for the most important job interview of your life,- possible, but rarely optimal.

2. Buyer identification and outreach.

An experienced advisor maintains a database of active buyers,- strategic corporates, PE funds, family offices, HNIs, and competitor groups. They build a target list of 20-50 potential acquirers, approach them confidentially under NDA, and qualify their interest before you speak to anyone. You cannot replicate this from your office in Ahmedabad or Pune. The network is the product.

3. Competitive tension.

This is the single most valuable thing an advisor does. When 3-5 serious buyers are bidding at the same time, with the same deadline, each knowing the others exist,- the price goes up. In a bilateral conversation with one buyer, you have zero leverage. The advisor creates the auction that creates the leverage that creates the premium.

Pro Tip: Ask any advisor you interview: ‘How many qualified buyers do you typically bring to a deal in my sector and size range?’ If the answer is ‘a couple,’ keep looking. The whole point is competitive tension.

4. Valuation and deal structuring support.

The advisor helps you determine a defensible price range, models different deal structures (share sale vs slump sale vs earn-out), and advises on which structure optimises your post-tax proceeds. They work with your CA to ensure the tax modelling is correct and the valuation is defensible.

5. Due diligence management.

When the buyer’s DD team arrives, the advisor manages the virtual data room, coordinates document requests, shields your management team from excessive disruption, and ensures that findings are contextualised before they become price renegotiation ammunition.

6. Negotiation.

The advisor negotiates on your behalf,- not just the price, but the escrow, the earn-out targets, the non-compete scope, the representations and warranties, and every other clause in the SPA that determines how much money you actually take home. They have done this dozens of times. You are doing it once. That experience gap is worth crores.

7. Deal coordination and closing.

The advisor coordinates between your lawyer, CA, the buyer’s team, and regulators (CCI, NCLT, SEBI, RBI as applicable) to keep the deal on track and on timeline. Deals that lose momentum die. The advisor’s job is to keep momentum.

What It Costs: Advisory Fees in the Indian Market

Advisory fees in India are lower than global benchmarks but still represent a significant commitment. The ranges below are based on industry benchmarks and advisory practices observed in the Indian mid-market. No Indian advisory firm publishes standardised fee schedules,- actual fees vary by advisor, deal complexity, sector, and negotiation. Here is what to expect, with INR examples:

Fee Components

Retainer (monthly):

Rs.1-10 lakh per month, depending on deal size and advisor tier. Paid monthly for 6-12 months. Covers the advisor’s time for CIM preparation, buyer outreach, and process management. In most Indian engagements, the retainer is credited against the success fee,- meaning it is an advance, not an additional cost.

Success fee (paid at closing):

1-3% of the total deal value. This is the largest component. Paid only if the deal closes. The percentage decreases as deal size increases,- 3% on a Rs.10 crore deal, 1.5-2% on a Rs.50 crore deal, 1% or less on Rs.100 crore+ deals.

Minimum fee:

Most advisors have a floor. For boutique M&A advisors in India, this is typically Rs.15-30 lakh. For investment bankers, Rs.50 lakh-1 crore. The minimum ensures the advisor is compensated even on smaller deals that require substantial work.

Expense reimbursement:

Travel, data room, third-party reports. Usually capped at Rs.2-5 lakh. Negotiate the cap upfront.

| WHAT IT LOOKS LIKE IN PRACTICE Rs.10 crore deal: Retainer Rs.1 lakh/month x 8 months = Rs.8 lakh. Success fee at 3% = Rs.30 lakh. Retainer credited. Total: Rs.30 lakh. The 15-25% price uplift from competitive auction = Rs.1.5-2.5 crore. Net gain after advisory fee: Rs.1.2-2.2 crore. Rs.50 crore deal: Retainer Rs.2.5 lakh/month x 10 months = Rs.25 lakh. Success fee at 2% = Rs.1 crore. Retainer credited. Total: Rs.1 crore. Price uplift from auction: Rs.7.5-12.5 crore. Net gain: Rs.6.5-11.5 crore. The maths is clear: the advisory fee pays for itself many times over in a competitive process. The only scenario where it does not is when the advisor fails to create competitive tension,- which is why choosing the right advisor matters more than negotiating the fee. |

Pro Tip: Always negotiate for the retainer to be credited against the success fee. Most Indian advisors agree to this. If they refuse, ask why,- it may indicate they are not confident in closing the deal.

| NOT SURE IF YOU NEED AN ADVISOR? Every deal is different. A 15-minute conversation can clarify whether your deal size, complexity, and timeline warrant advisory support,- or whether a good CA is all you need. Talk to us: [email protected] | 8000 422 133 |

When You Do NOT Need an Advisor (Honest Answer)

Not every deal needs an M&A advisor. Here are the situations where you can probably do without one:

The buyer is already identified and the relationship is strong.

If your largest customer, a trusted competitor, or a family friend has approached you with a serious offer, and the relationship is genuine,- adding an advisor can sometimes introduce friction rather than value. The deal is relationship-driven, and the negotiation is collaborative rather than competitive.

The deal is below Rs.5 crore and the structure is simple.

A straightforward share purchase of a small private company, with a single buyer and no regulatory complexity, may not justify advisory fees. A CA with M&A experience can handle the valuation, tax structuring, and SPA review at a fraction of the cost.

You are doing a management buyout with your own team.

If your management team is buying the business, the negotiation is internal. You need a valuer, a lawyer, and a tax advisor,- not an M&A process. The relationship dynamics are different from an external sale.

But here is the honest caveat.

| “Never sell without an advisor when dealing with a PE firm. PE firms are very savvy with their investments. Their entire process is about purchasing something for as low as they can get it. They know the tricks to drive down the price.” By Linda Rose, Founder & CEO, CPA, Author of ‘Get Acquired for Millions’, RoseBiz Inc Source: RoseBiz |

If your buyer is a PE firm, a large corporate, or any entity that has a professional M&A team on their side,- you need one too. The asymmetry in experience, process knowledge, and negotiation sophistication will cost you far more than the advisory fee.

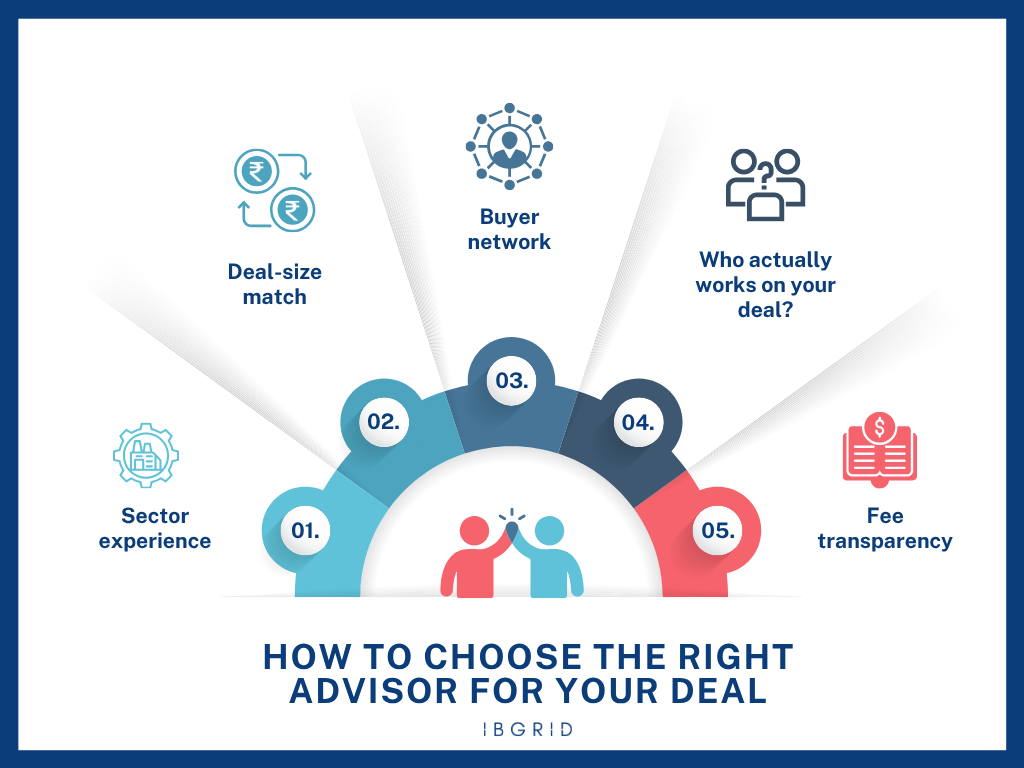

How to Choose the Right Advisor for Your Deal

Five criteria separate a good advisor from one who costs you time, money, and deal certainty:

1. Sector experience.

An advisor who has closed deals in your industry understands your value drivers, knows who the likely buyers are, and can tell your story in the language buyers respond to. A generalist who has never sold a manufacturing business will struggle to position yours correctly,- regardless of their credentials.

2. Deal-size match.

An advisor who typically handles Rs.500 crore deals will treat your Rs.20 crore deal as an afterthought. Conversely, a small CA firm is not equipped to run a Rs.100 crore auction. Match the advisor to your deal size. Ask: what is the average deal value you have closed in the last 2 years?

3. Buyer network.

The advisor’s value is directly proportional to the number of qualified buyers they can bring to your deal. Ask for specifics: how many buyers in my sector are in your active database? How many deals have you closed with PE firms vs strategic buyers? If they cannot answer with numbers, they are selling confidence, not capability.

4. Who actually works on your deal?

In larger advisory firms, the senior partner sells the engagement and a junior analyst runs the day-to-day. This is the single most common complaint from business owners who hired investment banks. Ask explicitly: who will be my primary point of contact? How many deals is that person currently running? Will the senior person who pitched me stay involved?

Pro Tip: Ask to speak with 2-3 previous clients who sold businesses similar to yours in size and sector. Any advisor worth their fee will happily provide references. If they hesitate, that tells you everything.

5. Fee transparency.

Before signing the engagement letter, ensure you understand: the retainer amount and whether it is credited against the success fee, the success fee percentage and how it is calculated (on total enterprise value or equity value?), the minimum fee, the expense cap, and the tail period (how long after the engagement ends the advisor is still entitled to a fee if a deal closes with a buyer they introduced). Ambiguity in the engagement letter always favours the advisor, not you.

3 Mistakes That Cost Business Owners Crores When Choosing an Advisor

1. Choosing the cheapest option.

A CA who charges Rs.2 lakh to ‘help sell your business’ and an M&A advisor who charges Rs.30 lakh are not offering the same service. The CA will list your business passively and wait for a buyer. The advisor will build a CIM, identify 30+ targets, create competitive tension, and negotiate the SPA. The Rs.28 lakh difference in fee typically generates Rs.2-5 crore in additional deal value. Cheap advisory is the most expensive mistake in M&A.

2. Choosing a generalist.

An advisor who sold a restaurant last month and a logistics company the month before does not understand your industry’s value drivers, buyer universe, or deal dynamics. Sector specialisation is not a nice-to-have. It is the difference between an advisor who can tell your story and one who cannot.

3. Choosing an ‘elephant’,- an advisor too big for your deal.

Large investment banks occasionally take on smaller deals to fill pipeline gaps. But your Rs.20 crore deal will never get the same attention as their Rs.500 crore mandate. The senior partner who pitched you disappears. A junior analyst runs your process with minimal supervision. The deal drags. Buyers lose interest. Six months later, you are worse off than when you started,- because the advisor consumed your time, your exclusivity window, and possibly your best buyer’s patience. Match the firm to your deal. Not the other way around.

The 5 Questions Every Business Owner Asks Before Hiring an Advisor

How long does the sale process take with an advisor?

Typically 6-12 months from engagement to closing. The advisor spends 1-2 months on preparation and CIM, 2-3 months on buyer outreach and initial discussions, 2-3 months on DD and negotiation, and 1-2 months on closing and regulatory approvals. Rushing the process usually means less competitive tension and a lower price.

Can I switch advisors mid-deal?

Yes, but it is expensive and disruptive. Most engagement letters include a 60-90 day notice period and a tail clause (12-24 months during which the original advisor earns a fee if a deal closes with a buyer they introduced). Switching mid-process also resets relationships with buyers who were already engaged. The better approach: choose carefully upfront. Interview 3-5 advisors before signing.

What if the deal does not close? Do I still pay?

You pay the retainer regardless (it covers work performed). You do not pay the success fee unless the deal closes. This is why the retainer-credited-against-success-fee structure is important,- if the deal closes, the retainer was an advance. If it does not, the retainer is your total cost. Expenses (travel, data room) are usually reimbursable regardless of outcome.

Do advisors work for buyers too?

Yes. Buy-side advisory is common, especially for PE funds and corporate acquirers who want help identifying and evaluating targets. The same advisor should never represent both buyer and seller in the same deal,- that is a conflict of interest. Always confirm that your advisor does not have an existing relationship with the buyer that could compromise their loyalty to you.

Is the retainer refundable if I change my mind?

Generally, no. Retainers compensate the advisor for work already performed (CIM preparation, buyer research, market analysis). Most engagement letters specify that retainers are non-refundable. This is standard practice and not negotiable in most cases. What is negotiable is the retainer amount, the crediting mechanism, and the engagement term.

| READY TO EXPLORE YOUR OPTIONS? The right advisor turns your sale into a competitive auction. The wrong one turns it into a waiting game. The difference is crores. Book a free 30-minute consultation. We will help you assess whether advisory is right for your deal, what it should cost, and what to look for in an engagement letter. No pitch. No obligation. Just clarity. Email: [email protected] | Phone: 8000 422 133 |

One Reply to “Do You Need an Investment Banker to Sell Your Business in India?”