Every mistake on this list has destroyed real deal value in real Indian transactions. Most are preventable. All are expensive. This is the guide that tells you what goes wrong, and how to make sure it does not happen to your deal.

Why Most M&A Deals Fail And Why Indian Deals Fail Differently

A large scale analysis published in MIT Sloan Management Review in February 2026, covering thousands of deals by S&P 500 companies over 25 years, found that 46% of all M&A deals are ultimately undone, and the average time from acquisition to divestiture is a full decade.

Nearly half of all deals. Unwound. After years of effort, disruption, and cost.

| “Implementing best practice in M&A is very often what separates long-term value creation from value destruction. Where mergers and acquisitions are concerned, process is everything.” By Kison Patel, Founder & CEO, DealRoom / M&A Science (20+ years as M&A advisor, 400+ podcast episodes with practitioners), M&A Science Source: Kison Patel on LinkedIn |

Global deals fail for global reasons, synergy over optimism, cultural clashes, integration neglect. But Indian deals have their own failure patterns layered on top: informal business practices that surface during due diligence, regulatory timelines that nobody budgeted for, family dynamics that complicate governance, related-party transactions that buyers refuse to accept, and a tax landscape where the wrong deal structure can cost crores in avoidable liability.

Here are the 10 mistakes we see most often, and what each one actually costs.

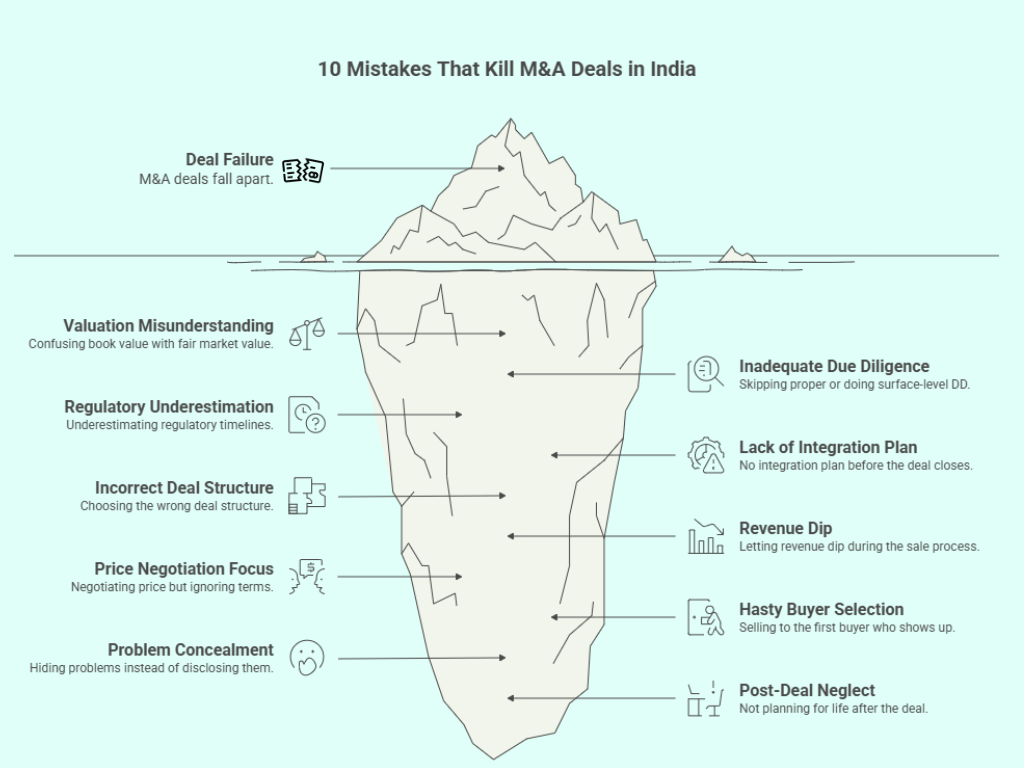

Mistake 1: Confusing Book Value with Fair Market Value

A manufacturing company in Pune has Rs.16 crore in net assets on its balance sheet. The promoter believes the company is ‘worth’ Rs.16 crore. A buyer runs a DCF analysis and values the business at Rs.34 crore based on future cash flows. Another buyer applies a 6x EBITDA multiple and arrives at Rs.28 crore.

The book value and the fair market value of a business are almost never the same number.

Business owners who anchor on book value either undervalue their company (leaving crores on the table) or overvalue it (scaring away serious buyers who know the real numbers). Before entering any M&A conversation, get an independent valuation from an IBBI-Registered Valuer or SEBI Merchant Banker using DCF, comparable transactions, and asset-based approaches. The valuation report costs Rs.1.5-5 lakh. Entering negotiations without one costs multiples of that.

Mistake 2: Skipping Proper Due Diligence (Or Doing Surface-Level DD)

Due diligence is where deals get repriced, restructured, or killed. And the most common reason Indian mid-market deals collapse after the LOI is signed is that the buyer discovers something during DD that the seller did not disclose or did not know about.

Daiichi Sankyo’s $4.6 billion acquisition of Ranbaxy is the most cited Indian DD failure. Post-acquisition, US FDA and DOJ investigations revealed fabricated drug testing data that was not disclosed during due diligence. Daiichi eventually received $525 million in arbitration, but the reputational and financial damage far exceeded the settlement. The case is documented in detail on iPleaders.

Pro Tip: Sellers: run your own sell-side DD before going to market. Every problem you find and fix before the buyer’s team arrives is a problem that does not reduce your price or kill your deal. The cost of sell-side DD is Rs.2-5 lakh. The cost of problems discovered by the buyer during DD is typically Rs.50 lakh-2 crore in price reductions and escrow demands.

Mistake 3: Underestimating Regulatory Timelines

Indian M&A involves a regulatory gauntlet that most business owners do not anticipate until they are already in the middle of it. NCLT schemes of arrangement take 6-12 months. CCI Phase I review takes 30 working days (Phase II can extend to 210 days). SEBI open offers for listed companies take 2-4 months. RBI approvals for cross-border deals under FEMA can take 3-6 months on the government route.

When these timelines are not factored into the LOI and deal schedule, the consequences cascade: the buyer’s financing window expires, the seller’s business performance dips under prolonged uncertainty, key employees start looking for other jobs, and the deal momentum dies. More Indian deals die from timeline exhaustion than from price disagreement.

Pro Tip: Before signing the LOI, map every regulatory approval your deal requires and build the timeline into the agreement. If your deal needs both CCI and NCLT, you are looking at 9-18 months, not the 4-6 months most owners expect.

Mistake 4: No Integration Plan Before the Deal Closes

Research published by Wharton’s Knowledge at Wharton in December 2025 identifies the most common integration failures: synergy overoptimism, timeline unrealism, missing dis-synergies (like customer losses and talent departure), and treating culture as an HR issue rather than a strategic imperative.

Tata Steel’s $12 billion acquisition of Corus is the Indian case that illustrates this most painfully. Post-acquisition, Tata invested over Rs.12,000 crore in Corus, manufacturing output fell from 18 mtpa to 10 mtpa, and Corus added $6 billion to Tata’s debt. The integration challenges, combining Indian and European operations, cultures, and cost structures, were underestimated at every stage. The case is documented on iPleaders (blog.ipleaders.in).

Integration planning must start before the deal closes, not after.

Budget 5-10% of the deal value for integration costs. Appoint a dedicated integration lead. Identify the top 10 customers and key employees who need personal communication on Day 1. And plan for cultural differences, if the buyer runs a corporate process and you ran an entrepreneurial shop, friction is inevitable unless you plan for it deliberately.

Mistake 5: Choosing the Wrong Deal Structure

Indian law offers multiple deal structures, share purchase, slump sale, scheme of arrangement, and asset purchase, and each has fundamentally different tax consequences.

On a Rs.25 crore share sale of an unlisted company held for more than 24 months, LTCG at 12.5% results in approximately Rs.3.12 crore in tax. The same transaction structured as an asset purchase, with depreciable machinery, inventory, and intellectual property, can trigger Rs.5-7 crore in combined capital gains, GST, and stamp duty.

That Rs.2-4 crore difference is the cost of not getting independent tax advice before agreeing to a structure.

The deal structure should be decided with your CA and M&A advisor before you negotiate the price, because the structure determines how much of the headline price you actually keep.

Mistake 6: Letting Revenue Dip During the Sale Process

This is the silent deal-killer that nobody writes about.

The sale process is consuming. Management is distracted by DD document requests, buyer meetings, and legal negotiations. The founder’s attention shifts from running the business to selling it. And during those 6-9 months, revenue dips, key client relationships weaken, and pipeline slows down.

Buyers track your performance in real time during DD. A 10-15% revenue dip between the LOI and closing is grounds for repricing, or walking away entirely. The buyer’s logic is simple: if the business cannot maintain performance during the sale, what happens after the founder leaves?

Pro Tip: Delegate the sale process to your M&A advisor and lawyer. Your job during the sale is to run the business at full intensity, not to manage the transaction. Every hour you spend on DD documents instead of client meetings costs you at both ends: the business weakens and the deal weakens.

| PLANNING A DEAL? AVOID THESE MISTAKES BEFORE THEY COST YOU. A 20-minute conversation can identify which of these 10 risks apply to your specific transaction, and what to do about each one. Talk to us: [email protected] | 8000 422 133 |

Mistake 7: Negotiating Price but Ignoring Terms

The price is the number you celebrate. The terms are the numbers that determine what you actually take home.

Earn-outs (15-30% of deal value tied to post-deal performance targets), escrow holdbacks (10-20% parked for 12-24 months against undisclosed liabilities), non-compete clauses (2-4 years, enforceable in post-sale contexts in India), and representations and warranties (personal liability for 3-7 years if anything you stated turns out to be untrue), these terms collectively determine whether your Rs.50 crore headline price results in Rs.50 crore in your account or Rs.35 crore with Rs.15 crore tied up in conditions.

Negotiate every term with the same intensity you negotiate the price. Better yet, have your M&A advisor negotiate the terms, they have done it dozens of times and know where to push and where to concede.

Mistake 8: Selling to the First Buyer Who Shows Up

A friendly competitor calls. They make what sounds like a reasonable offer. The promoter, tired, ready to move on, relieved that someone is interested, accepts without testing the market.

This is how business owners leave 15-25% of their deal value on the table.

A structured sale process, where your M&A advisor approaches 20-50 potential acquirers, qualifies 5-10 serious parties, and runs a competitive auction with a deadline, creates the leverage that a bilateral conversation cannot. When 3-5 buyers are bidding at the same time, each knowing the others exist, the price goes up. Without competitive tension, the buyer sets the price. With it, you do.

Even if you already have a buyer in mind, running a limited market check with 5-10 alternative buyers provides validation that the offer is fair, or reveals that significantly better offers exist.

Mistake 9: Hiding Problems Instead of Disclosing Them

Undisclosed income tax demands. GST input credit mismatches. Related-party transactions at non-arm’s-length prices. Verbal contracts with major customers. A consumer case in a district forum. A show-cause notice from the pollution control board sitting in a drawer.

Every one of these problems will be discovered during due diligence. The question is not whether the buyer finds them, it is how they react when they do.

When the seller proactively discloses a problem, provides context and a resolution plan, and builds it into the deal structure upfront, the impact is manageable, a Rs.10 lakh consumer case that you disclosed costs you almost nothing in credibility. The same case discovered by the buyer’s lawyer during DD costs you Rs.50 lakh in escrow, a repriced deal, and a relationship that now operates on suspicion rather than trust.

Pro Tip: Disclosure is always cheaper than discovery. Run a sell-side DD, catalogue every issue, and present them to the buyer with context and remediation. The buyer is not looking for a perfect company, they are looking for a transparent seller.

Mistake 10: Not Planning for Life After the Deal

The deal closes. The money hits your account, minus escrow. And then what?

If you signed an earn-out, you are still working in the business, but you no longer own it. The decisions are no longer yours. The culture changes. Employees who reported to you now report to someone else. Clients call the new management. The earn-out targets that seemed achievable during negotiation now depend on decisions made by people you do not control.

If you signed a non-compete, you cannot start a competing business for 2-4 years. If you did not plan for what comes next, another venture, advisory work, philanthropy, retirement, the post-deal period can feel like a vacuum. The emotional transition from ‘founder’ to ‘former founder’ is one that almost nobody prepares for, and almost everybody struggles with.

Plan for the day after the deal with the same rigour you plan for the deal itself. Negotiate your post-deal role explicitly. Define earn-out targets that are within your control. Clarify the non-compete scope narrowly. And have a clear answer to the question: what do I do on Monday morning after the deal closes?

3 Questions Every Business Owner Asks

1. What percentage of M&A deals actually fail?

Academic research varies, but the figures are consistently sobering. An MIT Sloan Management Review study (February 2026) found that 46% of deals by S&P 500 companies are ultimately undone. Fox Mandal, an Indian law firm, cites a Harvard Business Review figure of 70-90% of deals failing to achieve their intended objectives. The precise number depends on how ‘failure’ is defined, outright collapse, value destruction, or simply not meeting synergy targets, but the directional message is clear: M&A failure is the norm, not the exception.

2. When do most deals collapse?

Most mid-market deals collapse during due diligence (problems surface that were not anticipated) or during the gap between LOI and definitive agreement (the parties cannot agree on terms, the regulatory timeline extends, or the business deteriorates during the process). Deals that make it past the definitive agreement rarely collapse, but they may still fail to create value if integration is poorly executed.

3. How do I avoid these mistakes?

Start with preparation: independent valuation, sell-side DD, clean financials, formalised contracts. Engage the right advisor for your deal size. Map the regulatory timeline before signing the LOI. Negotiate terms, not just price. Run a competitive process. Disclose everything. Plan for integration before closing. And plan for your own life after the deal. Every mistake on this list is preventable, if you address it before the process starts, not after.

| AVOID THE MISTAKES THAT KILL DEALS. Every mistake on this list has a cost measured in crores. Every one of them is preventable with the right preparation and advice. Book a free 30-minute consultation. We will assess your deal, identify which of these risks apply, and help you build a plan to address them before they become expensive. No pitch. No obligation. Just a clear-eyed assessment. Email: [email protected] | Phone: 8000 422 133 |

One Reply to “10 Mistakes That Kill M&A Deals in India”