What your business is worth, how to find out, which Indian regulations demand it, and the mistakes that quietly cost owners crores every year.

Every major business decision,- selling the company, bringing in an investor, buying out a partner, issuing ESOPs, or even filing certain tax returns,- eventually comes down to one question: what is this business actually worth?

The answer is not on your balance sheet. Your balance sheet shows book value,- what you paid for assets minus depreciation. A factory built for Rs.10 crore in 2012 might show Rs.4 crore today, while its replacement cost is Rs.15 crore and the business running inside it generates Rs.40 crore in lifetime cash flows.

Business valuation closes that gap. It estimates the fair market value of your company,- what a willing buyer would pay a willing seller in an open market, with both sides fully informed. That number is what investors price their stakes on, what tax authorities use to assess your capital gains, and what acquirers negotiate against when they want your company.

| THE GAP IN PRACTICE An auto components manufacturer in Pune. Revenue: Rs.40 crore. PAT: Rs.4 crore. Balance sheet (book value): Rs.16 crore DCF-based fair market value: Rs.34 crore The Rs.18 crore difference is customer relationships, brand reputation, operational efficiency, and growth potential,- real value the balance sheet does not capture. If you walk into a negotiation quoting Rs.16 crore, you leave Rs.18 crore on the table. |

When Indian Law Requires You to Get Valued

Valuation in India is not just a good idea,- it is legally mandatory in more situations than most business owners realise. Missing a required valuation can mean penalties, rejected filings, or invalid transactions.

- Companies Act (Section 247): Preferential share allotment, mergers and demergers, non-cash director transactions, buybacks, ESOP grants, and voluntary liquidation all require a report from an IBBI-Registered Valuer. Penalty for non-compliance: Rs.50,000 on the valuer; if fraudulent: up to 1 year imprisonment and fine of Rs.1–5 lakh.

- Income Tax Act (Sections 50CA & 56(2)(x)): Any transfer of unquoted shares triggers FMV computation under Rule 11UA. Sell below FMV and the tax department deems FMV as your sale price. Buy below FMV and the shortfall is taxed as your income. Both sides get hit on the same transaction.

- FEMA / RBI: Every share issuance to a non-resident and every cross-border share transfer must be at fair market value, certified by a SEBI Merchant Banker or Practicing CA.

- SEBI: Listed company preferential issues, takeovers, buybacks, delisting, and AIF portfolio valuations all require independent valuation.

- IBC, 2016: Two IBBI-Registered Valuers must independently determine fair value and liquidation value during insolvency resolution, the only Indian regulation mandating dual valuation.

| ANGEL TAX IS GONE. THE OBLIGATION IS NOT. Section 56(2)(viib),- the Angel Tax,- was abolished from FY 2024-25 by the Finance Act, 2024. But Sections 50CA and 56(2)(x) remain fully operative for share transfers. Companies Act requirements for share allotments and ESOPs are untouched. FEMA pricing still applies for foreign investors. If someone tells you valuation is no longer needed post-Angel Tax, they are wrong. |

Five Methods, One Decision: Which One Fits Your Situation?

The right method depends on why you need the valuation, the nature of your business, and which regulation governs your situation. Using the wrong method is not just inaccurate,- it can make your report legally invalid.

| “Using the same valuation logic for different use-cases,- selling the business vs. issuing new shares vs. bank loans,- is one of the most common mistakes. Each requires different considerations and methods.” By Valuation Advisory, M&A and Valuation Practice, PKC India Source: PKCIndia.com |

| Your Situation | Best Method | Why This One | Regulation |

| Selling your company | EBITDA Multiple + DCF cross-check | Buyers benchmark multiples; DCF validates earning power | Commercial + IT Act |

| Raising capital (Indian investor) | DCF or Revenue Multiple (if pre-profit) | Investors want future cash flow potential | Companies Act S.62 |

| Raising capital (foreign investor) | DCF certified by SEBI MB or practicing CA | FEMA requires arm’s-length FMV for FDI pricing | FEMA NDI Rules + S.62 |

| IT compliance (share transfer) | NAV per Rule 11UA or DCF by merchant banker | Only two methods accepted by the Income Tax Act | S.50CA + S.56(2)(x) |

| Merger or demerger | DCF + NAV (dual approach) | NCLT expects robust justification from two methods | Companies Act S.230-232 |

| ESOP valuation | DCF or NAV | Determines exercise price; must be defensible for tax | Companies Act + IT S.17(2) |

| Partner buyout / succession | Capitalization of Earnings + NAV | Stable earnings suit capitalization; NAV covers asset base | Companies Act + IT Act |

| IBC insolvency resolution | DCF (fair value) + Liquidation Value | IBC mandates both; fair value as ceiling, liquidation as floor | IBC 2016 (two RVs required) |

| RULE OF THUMB Always use at least two methods and compare results. If they fall within 15-20% of each other, you have a defensible range. If they diverge sharply, the gap itself reveals something important about your business that needs investigation before you proceed. |

Quick Reference: What Each Method Actually Does

DCF (Discounted Cash Flow):

Projects your future free cash flows and discounts them to today’s value using your cost of capital (WACC). Captures earning potential. Best for companies with predictable cash flows. India WACC: typically 12-18% for mid-market companies.

NAV (Net Asset Value):

Total assets minus total liabilities per Rule 11UA formula. Simple, rule-based. Best for asset-heavy businesses and IT Act compliance. Limitation: ignores intangible value entirely.

EBITDA Multiple:

Your EBITDA times an industry-specific number. The common language of Indian M&A. IT services: 8–14x. Manufacturing: 5–8x. SaaS: 10–20x EBITDA (or 3–6x revenue if pre-profit). FMCG: 8–15x. These ranges vary significantly based on company size, growth rate, profitability, and buyer type — PE buyers typically pay higher multiples than strategic acquirers. Cross-reference with the latest Grant Thornton Dealtracker for current Indian multiples.

Comparable Transactions:

What did similar businesses sell for recently? Grounds your valuation in real deal data. Sources: VCCEdge, Tracxn, Grant Thornton Dealtracker, BSE/NSE disclosures.

Revenue Multiple:

Annual revenue times a sector multiple. Used for pre-profit startups. Post the 2021-22 correction, SaaS revenue multiples settled from 15-40x to 3-7x by 2025-26. Top-quartile companies with high retention and strong growth can still push 8-10x.

Four Mistakes That Quietly Cost Owners Crores

| “You’re definitely wrong. If your reaction is ‘I don’t want to be wrong,’ don’t value companies. Your consolation prize: you don’t have to be right. You just have to be less wrong than everybody else.” By Prof. Aswath Damodaran, Professor of Finance, NYU Stern School of Business Source: CFA Institute, Alpha Summit GLOBAL |

1. Treating your balance sheet as your valuation.

Book value reflects historical cost, not economic worth. For service businesses, tech companies, and any company where intangibles dominate, book value understates true worth by 3-10x. A buyer who hears you quote your book value assumes you don’t understand what you’re selling.

2. Relying on a single method:

NAV ignores future earnings. DCF depends on assumptions that can be challenged. EBITDA multiples vary by deal context. Every experienced valuer uses at least two methods. If yours used only one, push back and ask for a cross-check.

3. Inflating DCF projections to inflate the number:

Projecting 25-30% growth for a decade when your industry grows at 12% is the fastest way to get your report rejected by a tax authority, challenged by a buyer, or dismissed by an investor. Conservative base-case assumptions supported by industry data are always more defensible than optimistic hockey sticks.

4. Getting the wrong report for the wrong regulation:

A DCF signed by your CA without IBBI registration is invalid for Companies Act purposes. An NAV computation does not satisfy FEMA if the regulation requires DCF. A report for business fundraising may not meet Income Tax requirements. Always identify the regulation first, then commission the report. Not the other way around.

Who Can Legally Sign Your Report?

A report signed by the wrong professional is invalid,- and you will pay for it again. Here is the rule:

- Companies Act or IBC valuation: IBBI-Registered Valuer only (Securities or Financial Assets class). Your regular CA cannot sign this unless they have IBBI registration. Mandatory since February 2019.

- IT Act DCF route (Rule 11UA): SEBI-Registered Merchant Banker. An IBBI-RV alone is not accepted for DCF under Rule 11UA.

- IT Act NAV route (Rule 11UA): Can be self-computed by the company. No mandatory signatory. But a valuer’s sign-off adds defensibility against tax department challenges.

- FEMA / FDI pricing: SEBI Merchant Banker or Practicing Chartered Accountant. Must certify arm’s-length methodology.

Before engaging anyone, confirm the purpose of the report. The purpose determines the legally authorized signatory.

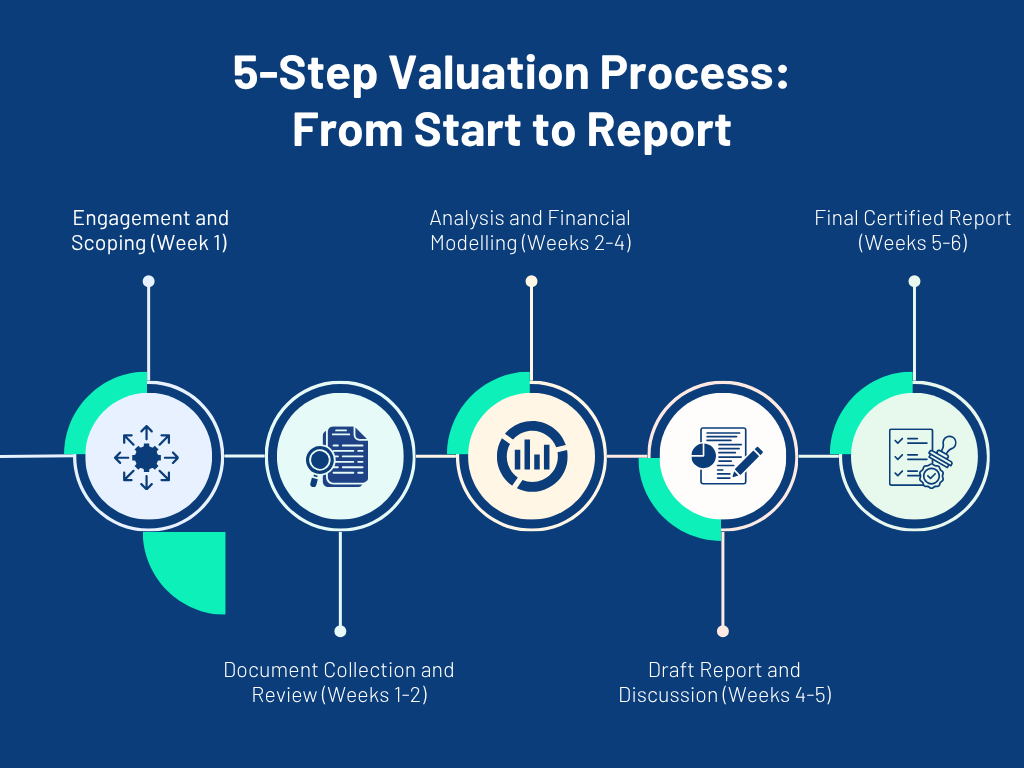

How the Valuation Process Works: 5 Steps From Start to Report

Most business owners have never been through a formal valuation. Here is exactly what happens, step by step, so there are no surprises.

- Step 1: Engagement and Scoping (Week 1)

The process starts with a conversation. You tell the valuer why you need the report,- fundraising, M&A, tax filing, ESOP, or strategic planning.

They define the scope: which entity is being valued, which asset class, what valuation date, and which regulation governs the report.

This scoping step is critical because it determines the method, the signatory, and the deliverable format. A valuation commissioned for the wrong purpose is money wasted.

Cost agreed at this stage: Rs.25,000, Rs.75,000 for a basic NAV of a small Pvt Ltd. Rs.1.5, 5 lakh for a full DCF of a mid-market company. Rs.10, 30 lakh+ for complex engagements (IBC, cross-border, multiple entities). - Step 2: Document Collection and Review (Weeks 1-2)

The valuer sends you a document request list. This is where most delays happen,- not because the valuer is slow, but because the business owner’s records are incomplete or scattered. Having these ready before you engage will cut your timeline by 2-3 weeks:

Financials: 3-5 years of audited income statements, balance sheets, and cash flow statements.

Tax records: IT returns, GST filings, TDS certificates, and any pending assessments or demands.

Corporate records: MOA/AOA, shareholder agreements, board resolutions, and up-to-date MCA annual filings.

Business documents: Key customer contracts, supplier agreements, lease/rental agreements, and ESOP plan if applicable.

Projections: 3-5 year revenue and expense forecasts with clearly stated assumptions,- not just a hockey stick in Excel.

The valuer reviews these documents, flags gaps, and asks follow-up questions. If your records are clean and audited, this step moves fast. If the valuer has to reconstruct your financials from raw data, add 3-4 weeks and expect a higher fee. - Step 3: Analysis and Financial Modelling (Weeks 2-4)

This is the core analytical work. The valuer normalises your financials,- adjusting for owner perks, related-party transactions at non-arm’s-length prices, one-time expenses, and accounting policy changes.

They build the valuation model (DCF, NAV, multiples, or a combination), benchmark against industry data, and stress-test key assumptions. For a DCF, this includes modelling your projected cash flows, selecting the discount rate (WACC), and computing the terminal value.

For an EBITDA multiple approach, they identify comparable transactions and apply the appropriate multiple with adjustments for size, growth, and risk. - Step 4: Draft Report and Discussion (Weeks 4-5)

You receive a draft valuation report with the preliminary value range, the methodology used, key assumptions, and supporting data.

This is your opportunity to review, ask questions, and flag anything the valuer may have missed,- a major customer contract renewal, a planned capex, or a pending litigation that affects value.

A good valuer welcomes this discussion. They want the report to reflect reality, not just the numbers in your financial statements. What they will not do is inflate the number to match your expectations,- the report must remain independent and defensible. - Step 5: Final Certified Report (Weeks 5-6)

After incorporating your feedback and finalising assumptions, the valuer issues the signed, certified valuation report. This is the document you submit to regulators (MCA, Income Tax, SEBI), present to investors, or use in M&A negotiations.

The report typically includes an executive summary with the concluded value or range, a description of the business and industry, the valuation methodology and rationale for method selection, detailed assumptions and sensitivity analysis, the valuer’s certification and credentials, and relevant disclaimers and limitations.

| TOTAL TIMELINE SUMMARY Basic NAV computation: 2-3 weeks end to end Standard DCF-based report: 4-6 weeks end to end Complex engagement (IBC, cross-border, multi-entity): 8-12 weeks end to end The single biggest factor that determines whether you finish in 3 weeks or 10 weeks is how organised your documents are on Day 1. Valuers do not charge by the hour for analysis,- they charge extra for doing your housekeeping. |

Quick Answers to the Questions You’re Still Asking

Only if they hold IBBI registration as a Registered Valuer (Securities or Financial Assets class). For FEMA/FDI pricing and certain IT Act filings, a practising CA is accepted. For Companies Act and IBC valuations, IBBI registration is non-negotiable since February 2019.

Every 12-18 months for strategic planning. Immediately before any triggering event,- fundraising, share transfer, ESOP grant, M&A, or regulatory filing. Annual valuations build a track record that strengthens your position in any future transaction.

Challenge the assumptions, not the conclusion. A good valuer presents a range (e.g., Rs.28-34 crore) and explains the growth rates, discount rates, and comparables behind it. You can question inputs. You cannot dictate the output,- the valuer must remain independent.

The tax on excess share premium (S.56(2)(viib)) was abolished from FY 2024-25. But Sections 50CA and 56(2)(x) for share transfers, Companies Act for share allotments, and FEMA for foreign investors all still require valuation. The premium tax is gone. The valuation obligation is not.

Reduce owner dependency. If your business cannot run without you for three months, every buyer, investor, and valuer sees concentrated risk and discounts accordingly. Build a management layer, systemise operations, and delegate relationships before going to market. This one change can add 15-30% to your multiple.

| READY TO GET YOUR BUSINESS VALUED? You now know why valuation matters, which method fits your situation, which regulations apply, and what mistakes to avoid. Book a free 30-minute consultation. We will assess your situation, recommend the right approach, and give you a clear scope, timeline, and cost estimate,- no obligation. Email: [email protected] | Phone: 8000 422 133 |

2 Replies to “Business Valuation in India: Methods, Process & When You Actually Need One”