This is the hardest conversation in any Indian family business. Not because the answers are complicated,- but because the question feels like planning for your own irrelevance. This guide makes it practical: the ownership structures, the tax implications, the governance tools, and the emotional reality nobody writes about.

The Conversation Nobody Wants to Have

Three numbers tell the story of Indian family businesses:

| THE SUCCESSION PARADOX Over 75% of India’s GDP comes from family-owned businesses 15% of those businesses have a documented succession plan. ~70% do not survive the transition to the second generation, according to industry research. |

Read those numbers together. The businesses that power India’s economy are the same ones most likely to collapse when the founder steps back. Not because the business fails. Because the family did not plan for what happens next.

The reason is rarely ignorance. Most founders know they need a succession plan. They defer it because the conversation forces them to confront uncomfortable truths: that they are not permanent, that their children may not want what they built, that equal does not mean fair when dividing a business, and that letting go of control is harder than building the company in the first place.

| “The Indian mindset is focused on having control, which comes with being involved in the management and taking decisions. Leaving the running of the business to a professional is not going to be easy for Indian promoters.“ By Gautami Gavankar, President, Kotak Mahindra Bank (formerly CEO, Estate Planning & Trusteeship Services, Kotak Mahindra Trusteeship Services) Source: Hubbis |

This guide is for founders ready to have that conversation.

Two Successions, Not One: The Distinction Most Families Miss

Succession is not one problem. It is two,- and conflating them is the single most common mistake Indian family businesses make.

Ownership succession

Ownership succession is a legal and financial question. Who will hold the shares? How will they be transferred? What tax will be triggered? What rights come with those shares? This is solved by lawyers, CAs, and valuers through wills, trusts, share transfers, and agreements.

Management succession

Management succession is a leadership and capability question. Who will run the business day to day? Are they ready? Do they want to? What happens if they are not competent? This is solved by grooming, governance structures, and sometimes the hardest decision of all,- bringing in a professional CEO.

You can transfer ownership to your three children equally while appointing one as CEO and the other two as board members. You can retain ownership while handing management to a professional. You can sell ownership to PE while keeping management with the family. Each combination has completely different legal, tax, and emotional consequences.

| THE CRITICAL QUESTION Before you choose any structure, answer this: do you want to transfer ownership, management, or both? And to whom? Family, professional, or external buyer? Every other decision flows from this answer. |

Once you know what you are transferring, the next question is how,- and what it costs.

5 Ways to Transfer Ownership (And What Each Costs in Tax)

India does not have an inheritance tax. That is the good news. The bad news: depending on how you transfer ownership, you may still trigger capital gains tax, stamp duty, and compliance obligations that can cost the family crores if structured incorrectly.

| Method | How It Works | Tax Treatment | Best For |

|---|---|---|---|

| Gift (inter vivos) | Transfer shares or assets to family members during your lifetime. No consideration. | No tax on recipient for gifts from specified relatives (S.56(2)(x) exempts them regardless of amount). Gifting is not a “transfer” under S.47 — no capital gains for the giver. Stamp duty applies on immovable property. | Straightforward family transfers. Parent to child. Between spouses. Keeps it simple. |

| Sale to next gen | Sell shares to your children or family members at fair market value. | Capital gains tax for the seller: LTCG at 12.5% if listed shares held >12 months; >24 months for unlisted shares. If sold below FMV to non-relatives, S.56(2)(x) taxes the shortfall in the buyer’s hands. Sales to specified relatives below FMV are exempt. | When you need liquidity from the exit. Or when gifting is not possible due to non-relative recipients. |

| Family Trust | Create a private trust (Indian Trusts Act, 1882). Transfer shares/assets to the trust. Appoint trustees. Define beneficiaries and distribution rules. | Transfer to an irrevocable trust: may trigger capital gains for the settlor. Income taxed at maximum marginal rate (MMR) for indeterminate beneficiary trusts. For determinate trusts, taxed at each beneficiary’s slab rate. Stamp duty on property transfers. | Complex families. Multiple beneficiaries. Protection from creditors. Controlled distribution over time. Avoiding probate. |

| Will / Testament | Specify how shares, assets, and business interests are distributed after death. Takes effect only on death. | No tax at the point of inheritance (India has no inheritance tax). But when the heir eventually sells inherited assets, capital gains are computed from the original owner’s cost of acquisition. | Simple estates. Single successor. When the founder wants to retain full control during their lifetime. |

| ESOP / MBO | Transfer ownership to management team through ESOPs or a management buyout, funded by company cash flow or external debt. | ESOP: perquisite tax on exercise (S.17(2)), capital gains on eventual sale. MBO: share purchase taxed as capital gains for the seller. | When no family successor is available or willing. Preserves the business. Rewards loyal management. |

| THE TRAP MOST FAMILIES MISS India has no inheritance tax,- but S.56(2)(x) of the Income Tax Act taxes the recipient if property is received below fair market value, even from family. The exemption only applies to ‘specified relatives’ as defined in the Act (spouse, siblings, lineal ascendants/descendants, and certain in-laws). If you are transferring assets to a nephew, a cousin, or a family member who does not fall within the specified relative definition, the recipient will be taxed on the difference between FMV and the consideration paid. Get the relationship mapping right before you execute. |

When the Next Generation Does Not Want the Business

This is the unspoken crisis in Indian family businesses.

The founder spent 30 years building the company. The children went to IIM, worked at McKinsey, and want to start their own venture,- or simply do not want to run a manufacturing unit in an industrial estate. The founder feels betrayed. The children feel trapped. And the business sits in limbo because nobody can say the quiet part out loud.

If this is your situation, you have four options,- and none of them require the business to die:

1. Professional CEO with family board control.

Hire an experienced professional to run the business. The family retains ownership and board seats, sets strategy, and receives dividends,- but does not manage day to day. This is the most common solution for Indian family businesses that survive beyond the second generation. Industry practitioners estimate that a majority of successful multi-generational family businesses use some version of this hybrid model.

2. PE buyout with management continuity.

Sell a majority stake to a private equity firm. They bring professional management, capital for growth, and a defined exit timeline (typically 4-7 years). You receive liquidity. The business continues under new ownership with existing management. The family can retain a minority stake if they wish.

3. Strategic sale.

Sell the entire business to a competitor, customer, or industry player. Clean exit. Full liquidity. The business merges into a larger entity. This is the right choice when no family member wants to be involved at all,- and you want to maximise the financial return.

4. Management buyout (MBO).

Your senior management team buys the business, often funded by a combination of company cash flow, bank debt, and PE co-investment. The people who know the business best take over. You receive your exit price over time. The legacy continues with the team that helped build it.

The worst option is the unspoken fifth one: doing nothing, hoping the next generation will change their mind, and watching the business slowly decline because the founder is aging and no successor is being prepared.

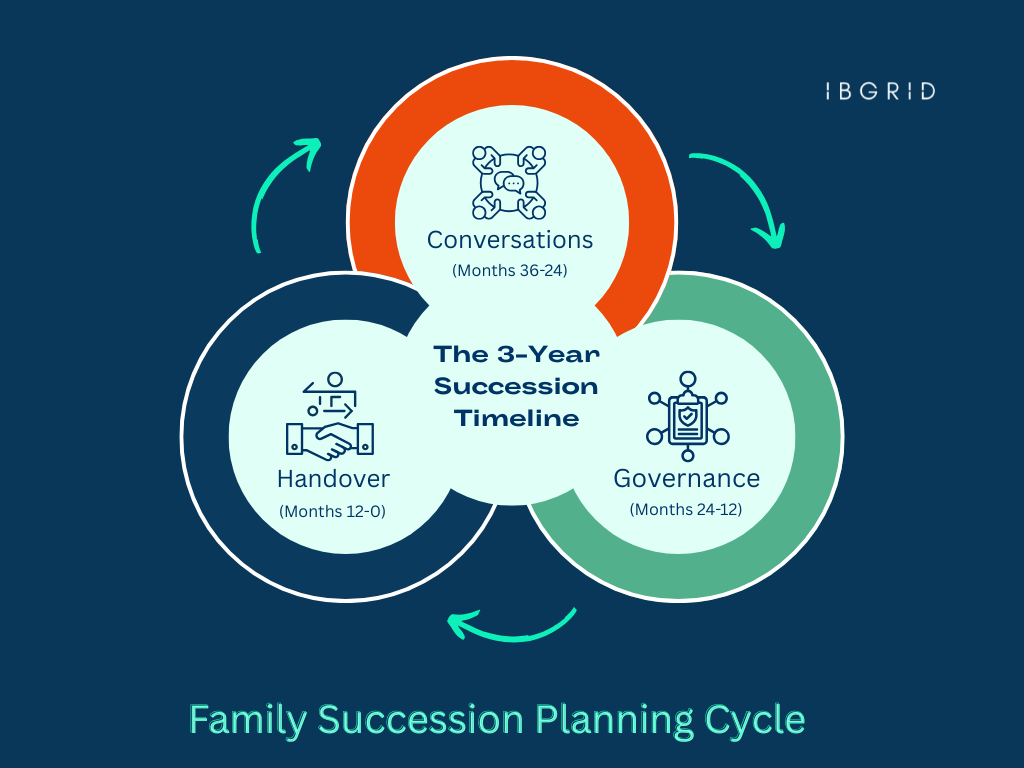

The 3-Year Succession Timeline: What to Do and When

| “Succession planning has moved from being a private, often deferred family matter to a mainstream strategic priority that promoters and patriarchs now address proactively. India is in the midst of an extraordinary generational wealth transfer estimated at $1.5 trillion over the next decade.” By Chambers & Partners, Succession & Estate Planning 2026, Chambers & Partners (India Practice Guide) Source: Chambers & Partners 2026 |

Year 3: The Foundation Conversations (Months 36-24)

Start with a family meeting,- not about legal documents, but about intent. What does the founder want after stepping back? What does each family member want? Is the next generation interested, capable, and willing? If there are multiple siblings, who leads,- and what do the others do? These conversations are uncomfortable. They are also the single most important step in the entire process. Skip them and every legal document you draft later will be built on assumptions that may be wrong.

Simultaneously, get an independent business valuation. Not to sell,- but to understand what you are transferring. If the business is worth Rs.50 crore, the succession plan looks very different than if it is worth Rs.5 crore. The valuation also becomes the baseline for any future gift, sale, or trust transfer.

Year 2: Structure and Governance (Months 24-12)

Draft the family constitution,- the non-binding governance document that codifies decision rights, employment criteria for family members, dividend policy, conflict resolution mechanisms, and exit conditions. This is not a legal agreement. It is a family agreement that becomes the operating manual for how the family interacts with the business.

Select and formally designate the successor,- whether family, professional, or hybrid. Begin the structured handover: the successor takes on increasing responsibility, sits in on key client meetings, attends board discussions, and starts making decisions with oversight. If the successor is external, negotiate their employment terms and governance role.

Engage a lawyer to draft the legal documents: updated will, shareholders’ agreement or buy-sell agreement, trust deed (if using a trust), power of attorney, and board resolutions authorising the succession-related decisions. Update the company’s Articles of Association to reflect any new governance provisions.

Year 1: Execution and Handover (Months 12-0)

Execute the ownership transfer,- whether by gift, sale, trust, or will (with the will taking effect on death, not during this period). File the necessary regulatory paperwork: ROC filings for director changes, share transfer forms, stamp duty payments, and tax filings for any capital gains triggered.

Communicate the transition to employees, key clients, suppliers, and bankers. This is not optional. Uncertainty kills morale and client confidence. The founder should personally introduce the successor to every important stakeholder and publicly endorse the transition.

The founder steps into an advisory or board role,- not an operational one. This is the hardest part. The temptation to override, to second-guess, to ‘just check in on that one client’ is enormous. Resist it. Every time you step back into the operational role, you undermine the successor’s authority and delay the transition by months.

The Family Constitution: Why It Matters More Than the Will

A will distributes assets after death. A family constitution governs how the family and the business interact while everyone is alive. For any family with two or more members involved in the business, the constitution is more important than the will,- because most succession disputes happen before death, not after.

A well-drafted family constitution typically covers:

Decision rights:

Who has authority over which business decisions? Who can hire, fire, approve expenditures above a threshold, enter new markets, take on debt?

Employment criteria:

Under what conditions can family members work in the business? Minimum qualifications? External experience requirement? Reporting to a non-family supervisor? Compensation benchmarked to market, not to family status?

Dividend and distribution policy:

How are profits shared between reinvestment and family withdrawals? What is the minimum dividend? What happens in a loss year?

Conflict resolution:

How are disagreements resolved? Family council? External mediator? Binding arbitration? The mechanism must be defined before the conflict occurs,- not during it.

Exit mechanisms:

If a family member wants out, how are their shares valued and purchased? Right of first refusal for other family members? Valuation methodology agreed in advance?

The constitution is non-binding in a legal sense. But families that have one report dramatically fewer disputes, smoother transitions, and stronger governance. It works because it converts unspoken assumptions into written agreements,- before emotions run high.

The Legal Documents You Actually Need

Every succession plan requires a set of legal and financial documents. Without proper documentation, even the best-laid plan can fail during execution. Here is what you need:

Will or testament:

Specifies how your shares, business interests, and personal assets are distributed upon death. Must comply with the applicable personal law: Hindu Succession Act (for Hindus, Sikhs, Jains, Buddhists), Indian Succession Act (for Christians, Parsis, and others), or Muslim personal law (Sharia-based fixed shares).

Note: the Hindu Succession (Amendment) Act, 2005 grants daughters equal coparcenary rights,- your succession plan must account for this.

Shareholders’ agreement / buy-sell agreement:

Defines share transfer rules, exit mechanisms, right of first refusal (ROFR), drag-along/tag-along rights, and what happens to shares on death, disability, or divorce. This is the operational backbone of ownership succession.

Family trust deed (if applicable):

Establishes the trust under the Indian Trusts Act, 1882. Names the settlor, trustees, and beneficiaries. Defines distribution rules, trustee powers, and succession of trusteeship. Irrevocable trusts offer stronger asset protection but less flexibility.

Power of attorney:

Authorises a trusted person to act on your behalf if you become incapacitated. Without this, the family may need a court order to manage business affairs during a medical emergency.

Board resolutions and updated AOA:

Formally approve succession-related decisions: director appointments, share transfers, governance changes. The company’s Articles of Association may need amendment to reflect new transfer restrictions or governance provisions.

3 Mistakes That Split Families and Kill Businesses

1. No written plan,- ‘everyone knows what I want.’

They do not. Verbal understandings are the leading cause of succession disputes in Indian families. What you told your eldest son in a private conversation is not what your youngest daughter understood from a family dinner. And none of it holds up in court. Write it down. Sign it. Get it witnessed. A succession plan that exists only in the founder’s head is not a plan,- it is a wish.

2. Treating all children equally, regardless of involvement.

Equal distribution feels fair. It is often the most destructive choice a founder can make. The child who runs the business 12 hours a day receives the same 33% as the child who moved abroad and has not attended a board meeting in five years. The operational child feels cheated. The absent child has voting power over decisions they do not understand.

The business becomes a battleground. The alternative: separate ownership from management compensation. The operational child receives a competitive salary plus management incentives. Ownership is distributed based on a family constitution that accounts for contribution, interest, and capability,- not birth order.

3. The founder who cannot let go.

This is the most human and most damaging mistake. The founder agrees to step back, announces the transition, and then continues to make decisions, override the successor, and hold court with employees who know where the real power still lies.

Every time this happens, the successor’s authority erodes, key employees hedge their bets, and the transition stalls. If you are not ready to step back, do not announce the transition. And if you have announced it, honour it. Your successor cannot lead a company while you are still running it from the next room.

The 5 Questions Every Family Business Owner Asks

Is there inheritance tax in India?

No. India abolished estate duty in 1985 and has not reintroduced inheritance tax. However, when the heir eventually sells inherited assets, capital gains tax applies,- computed from the original owner’s cost of acquisition and holding period. Additionally, transfers to non-specified relatives (as defined in the Income Tax Act) during the owner’s lifetime can trigger tax under S.56(2)(x). The absence of inheritance tax does not mean succession is tax-free.

What if my children disagree about who should run the business?

This is what the family constitution is for. Define the decision-making process, the successor selection criteria, and the conflict resolution mechanism before the conflict arises. If disagreement has already started, bring in an external facilitator,- a neutral advisor who has no stake in the outcome. Families that try to resolve succession disputes internally almost always make them worse.

When should I start planning?

Three years before you want the transition to be complete. Ideally, five. The families that start early have more options, better tax outcomes, and smoother transitions. The families that start in a crisis,- a health scare, a sudden death, a family fight,- have almost no good options left.

Do I need a family trust?

Not always. Trusts are most useful for complex families with multiple beneficiaries, large asset bases, minor heirs, or a desire to control distribution over time (e.g., releasing funds at age 25, 30, 35). For a straightforward parent-to-single-child transfer, a will plus a shareholders’ agreement may be sufficient. Trusts add complexity and cost,- use them when the situation warrants it, not as a default.

What about my daughter’s rights in the family business?

Under the Hindu Succession (Amendment) Act, 2005, daughters have equal coparcenary rights as sons in Hindu Undivided Family (HUF) property, including family business interests. Any succession plan that excludes or undervalues a daughter’s share is legally vulnerable to challenge. The law is clear: equal rights, regardless of gender. Your succession plan must reflect this,- both for legal compliance and for family equity.

| READY TO START THE CONVERSATION? Succession planning is not a single document. It is a process,- a series of conversations, decisions, and structures that unfold over years. The hardest part is starting. Book a free 30-minute consultation. We will help you map out your family’s situation, identify the right transfer structure, and create a clear timeline. No pressure. No judgment. Just a structured conversation to get you started. Email: [email protected] | 8000 422 133 |

One Reply to “Succession Planning for Indian Family Businesses – Complete Guide”